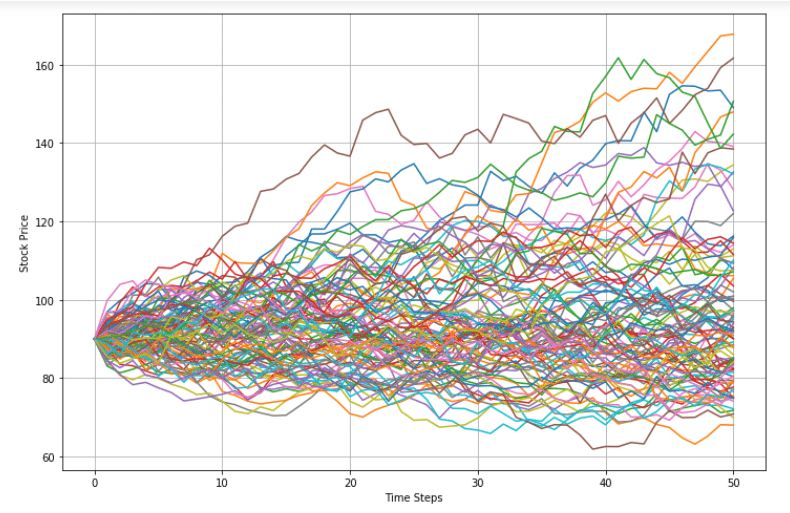

What Is The Monte Carlo Simulation. monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. what is monte carlo simulation? Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. The scientists are referring to monte carlo simulations, a statistical technique used to model probabilistic (or “stochastic”) systems and establish the odds for a variety of outcomes. While a simulation is a way to virtually demonstrate a strategy. monte carlo simulations, also called multiple probability simulations, are a modeling technique commonly used in the financial and. the monte carlo method uses a random sampling of information to solve a statistical problem; what does that mean? monte carlo simulation is a mathematical technique that estimates the possible outcomes of an uncertain event. This method uses random sampling to generate simulated input data and enters them into a

from marketxls.com

monte carlo simulation is a mathematical technique that estimates the possible outcomes of an uncertain event. what is monte carlo simulation? monte carlo simulations, also called multiple probability simulations, are a modeling technique commonly used in the financial and. The scientists are referring to monte carlo simulations, a statistical technique used to model probabilistic (or “stochastic”) systems and establish the odds for a variety of outcomes. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. what does that mean? the monte carlo method uses a random sampling of information to solve a statistical problem; While a simulation is a way to virtually demonstrate a strategy. This method uses random sampling to generate simulated input data and enters them into a

Monte Carlo Simulation Excel (with MarketXLS addin formulae)

What Is The Monte Carlo Simulation monte carlo simulations, also called multiple probability simulations, are a modeling technique commonly used in the financial and. While a simulation is a way to virtually demonstrate a strategy. monte carlo simulation is a mathematical technique that estimates the possible outcomes of an uncertain event. the monte carlo method uses a random sampling of information to solve a statistical problem; The scientists are referring to monte carlo simulations, a statistical technique used to model probabilistic (or “stochastic”) systems and establish the odds for a variety of outcomes. what does that mean? This method uses random sampling to generate simulated input data and enters them into a monte carlo methods, or monte carlo experiments, are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. monte carlo simulations, also called multiple probability simulations, are a modeling technique commonly used in the financial and. Monte carlo simulation uses random sampling to produce simulated outcomes of a process or system. what is monte carlo simulation?